Facing a mountain of debt can feel isolating and overwhelming, but taking proactive steps to resolve it is a powerful move toward regaining financial control. For many, a well-crafted Debt Negotiation Letter Template is the first and most crucial tool in this process. This formal communication opens a dialogue with your creditors, showing them you are serious about settling your obligations, even if you can't pay the full amount. It transforms a stressful situation from a series of harassing phone calls into a professional, documented negotiation.

This approach, also known as debt settlement, involves formally offering to pay a portion of your outstanding balance in a lump sum or through a structured payment plan. Creditors are often willing to consider such offers because receiving a partial payment is better than receiving nothing at all, which becomes a real risk if a debtor declares bankruptcy. A clear, concise, and professional letter sets the stage for a successful negotiation, demonstrating your intent and providing a clear starting point for discussions.

Navigating this process without guidance can be intimidating. What should you say? What information must you include? How do you make an offer that a creditor will actually consider? Understanding the key components of a settlement letter is essential. It's not just about asking for a discount; it's about presenting a realistic case based on your financial hardship and proposing a mutually beneficial solution.

This comprehensive guide will walk you through everything you need to know. We will break down the essential elements of a powerful negotiation letter, provide customizable templates for different scenarios, and offer strategic advice on how to manage the process from start to finish. By the end, you will have the confidence and the tools to write a letter that commands attention and puts you on the path to financial freedom.

Understanding Debt Negotiation Before You Write

Before you start drafting your letter, it's critical to understand what debt negotiation is and whether it's the right strategy for your situation. Debt negotiation, or debt settlement, is a process where a debtor negotiates with a creditor to pay back a reduced amount of their unsecured debt. Unsecured debts are those not backed by collateral, such as credit card balances, medical bills, and personal loans. Mortgages and auto loans are secured debts and are typically not eligible for this type of negotiation.

The primary goal is to reach a settlement agreement where the creditor accepts a one-time lump-sum payment that is less than the total amount owed. In return, the creditor agrees to forgive the remaining balance and report the account as "settled" or "paid as agreed" to the credit bureaus. While a lump-sum offer is most common and often preferred by creditors, some may be open to a structured payment plan if a single payment isn't feasible for you.

However, debt negotiation comes with significant trade-offs. The most notable downside is the potential impact on your credit score. When you stop making regular payments to save up for a lump-sum offer—a common strategy—your account becomes delinquent, which will lower your score. A "settled" mark on your credit report is also less favorable than an account "paid in full," but it is far better than a charge-off or bankruptcy. Furthermore, any forgiven debt over $600 may be considered taxable income by the IRS, so you could receive a 1099-C form and owe taxes on the amount that was canceled.

Key Elements to Include in Every Debt Negotiation Letter

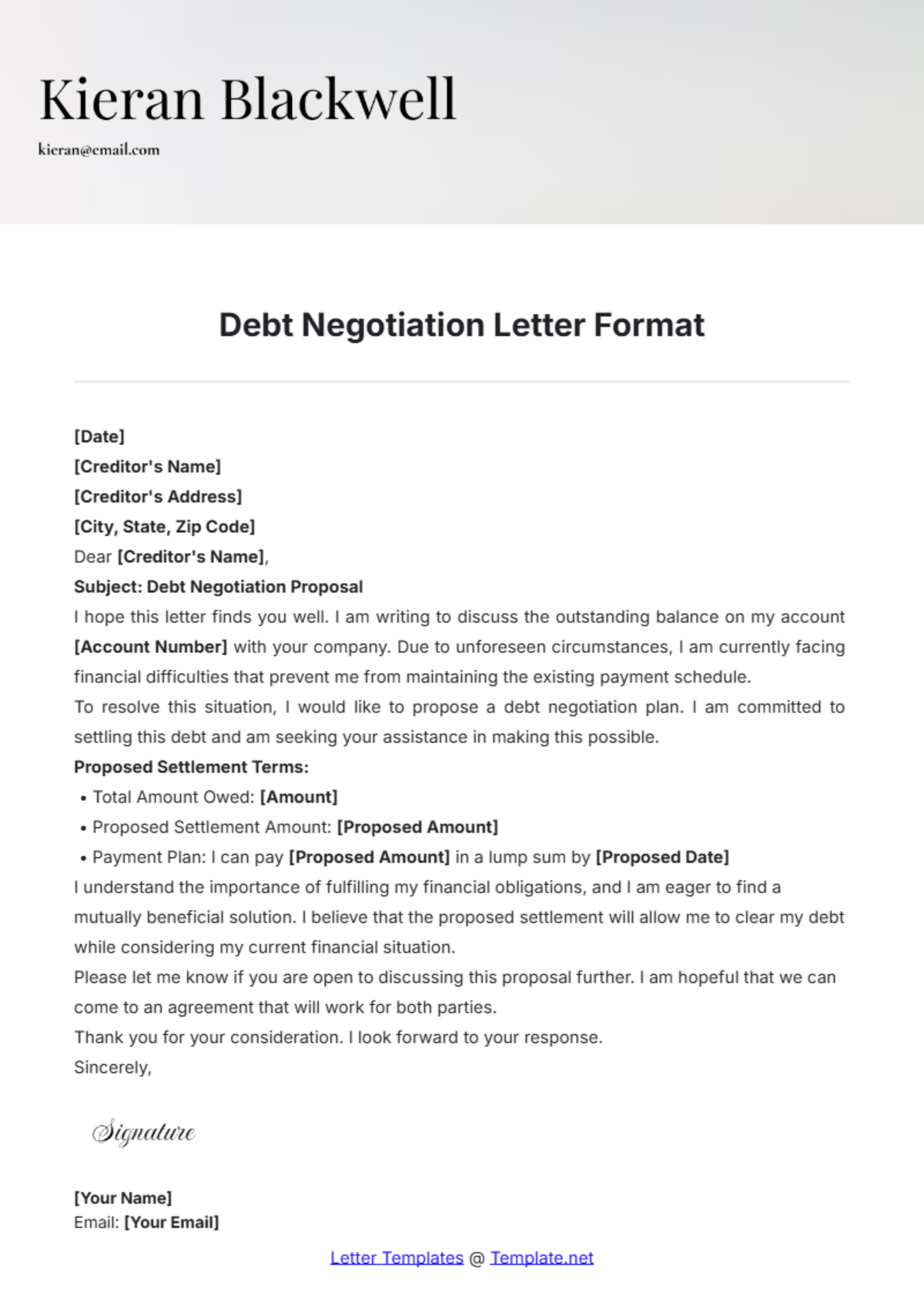

A successful negotiation letter is professional, clear, and contains all the necessary information for the creditor to make a decision. Omitting key details can lead to delays or an outright rejection of your offer. Every letter you send should be structured to include the following essential components.

Your Account Information

The very first thing a creditor needs to do is identify your account. Make this as easy as possible for them. At the top of your letter, clearly list your full name as it appears on the account, your current mailing address, and, most importantly, the specific account number you are writing about. This ensures your correspondence is routed to the correct department and linked to the right file without any confusion.

A Clear Statement of Your Financial Hardship

You need to briefly and honestly explain why you are unable to pay the debt in full. This is not the place for a long, emotional story. Instead, stick to the facts. Common reasons for financial hardship include job loss, a reduction in income, a medical emergency, divorce, or another significant life event that has impacted your finances. A simple sentence or two is sufficient. For example, "Due to a recent layoff, my income has been significantly reduced, and I am unable to meet my full debt obligations." This provides context for your offer without revealing unnecessary personal details.

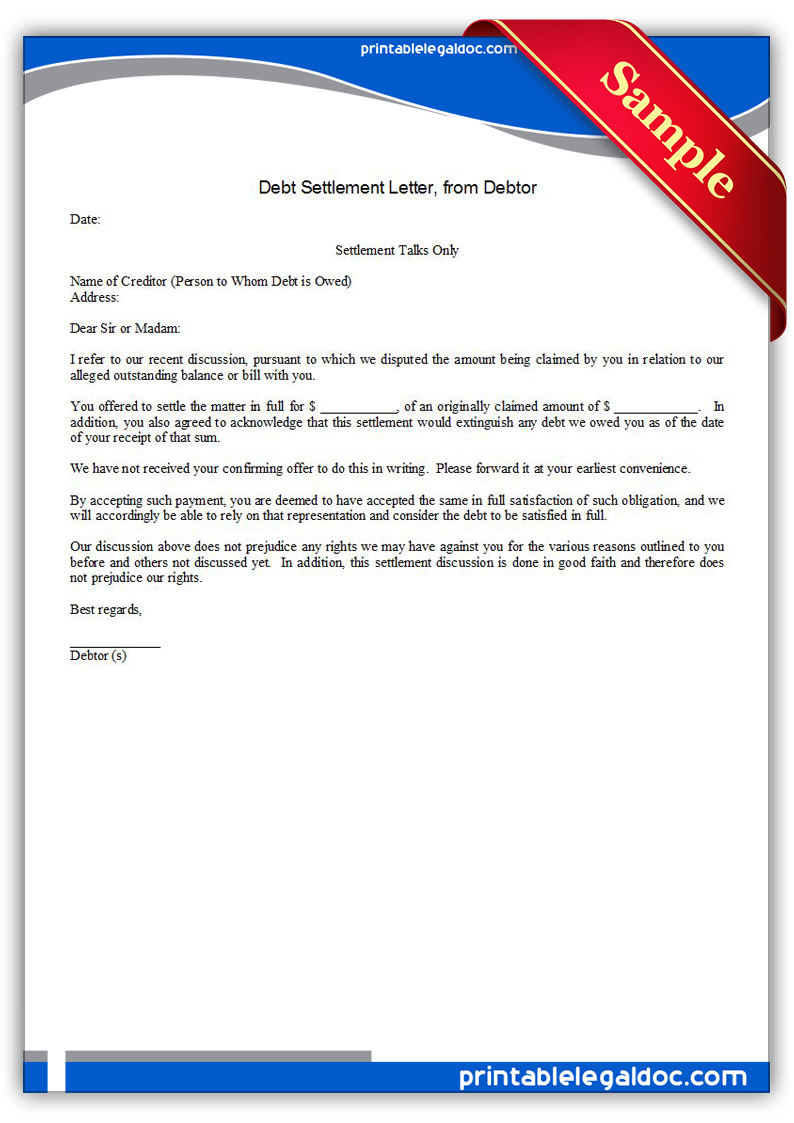

A Specific Settlement Offer

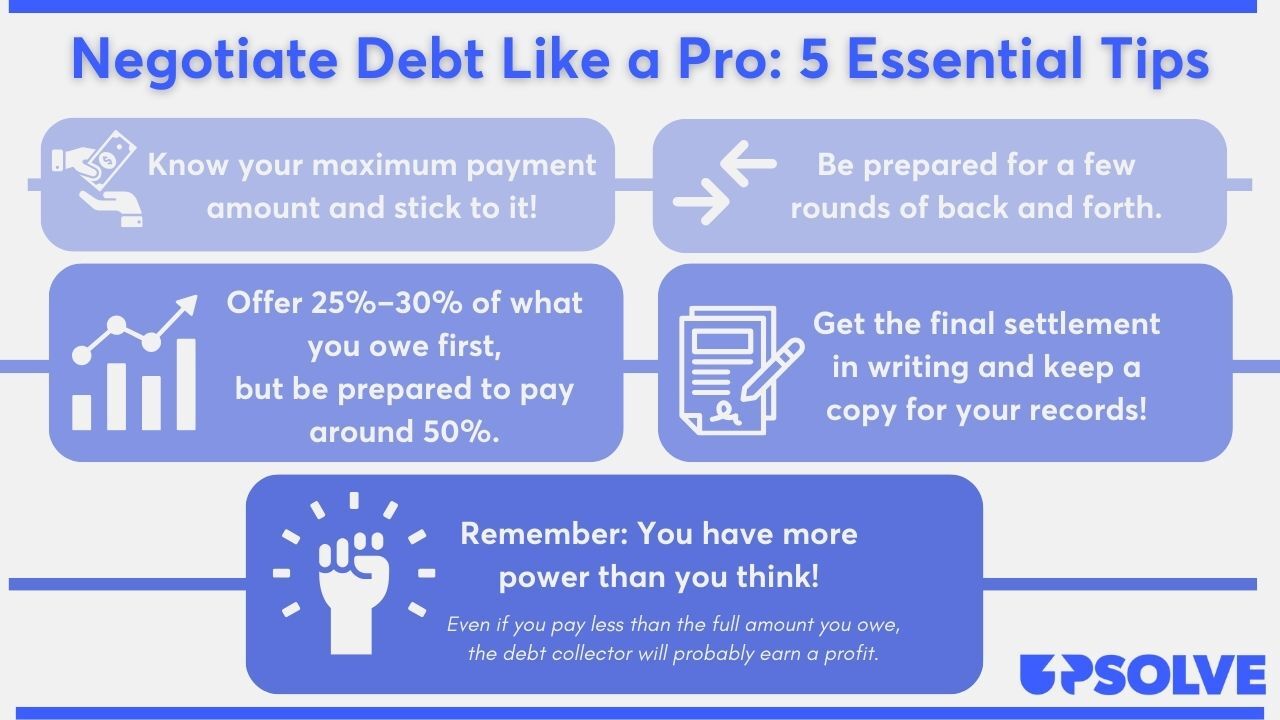

This is the core of your letter. You must propose a concrete solution. State the exact dollar amount you are offering to pay to settle the debt completely. This is typically a percentage of the total balance, with offers often starting between 25% and 50%. Your offer should be realistic and based on what you can actually afford. If you are making a lump-sum offer, state that the funds are available and can be paid promptly upon receiving a written agreement. If you are proposing a payment plan, outline the proposed monthly payment amount and the duration of the plan.

A Request for Written Agreement

This is a non-negotiable and critically important part of your letter. Explicitly state that your offer is contingent upon receiving a signed, written agreement from the creditor. This agreement should confirm that your payment will be accepted as settlement in full for the account and that they will cease all collection activities. Never send money based on a verbal promise. A written agreement is your legal protection and proof that the debt has been resolved.

A Deadline for Response

To encourage a timely reply and prevent your offer from being ignored, include a reasonable deadline. Typically, 15 to 30 days is an appropriate timeframe. State that if you do not hear back by that date, you will assume your offer has been rejected. This creates a sense of urgency and prompts the creditor to act on your request.

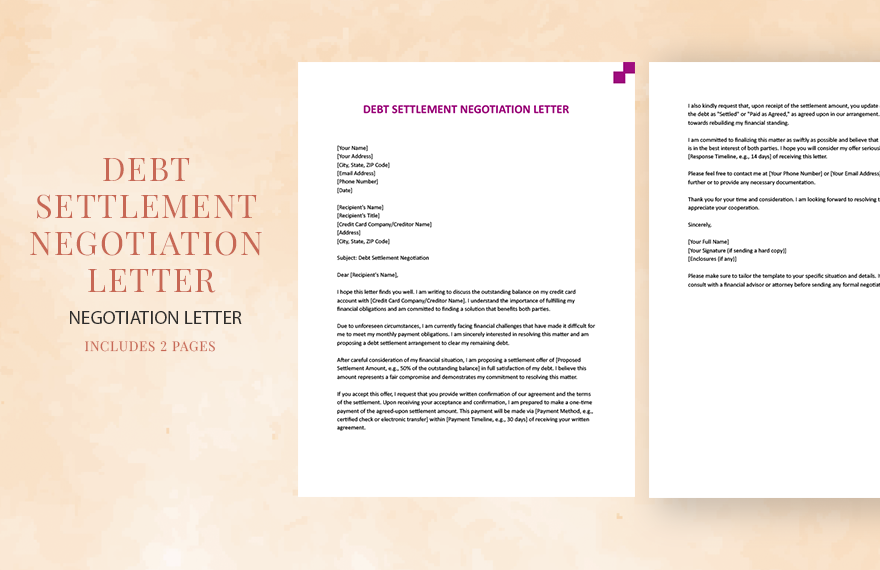

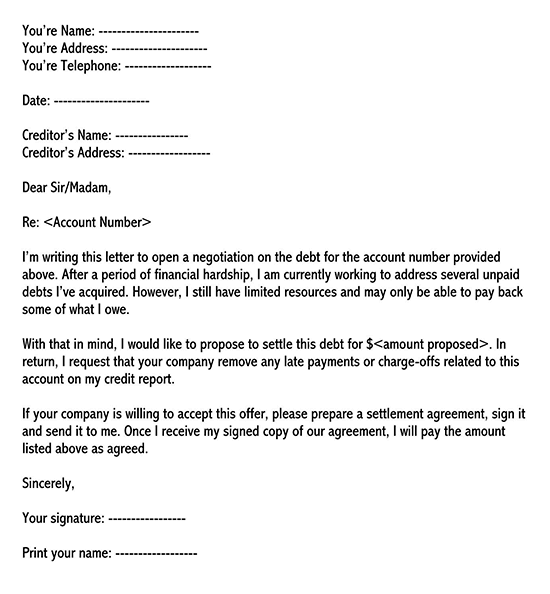

The Ultimate Debt Negotiation Letter Template: Lump-Sum Offer

When you have access to a sum of cash—perhaps from savings, a tax refund, or a loan from family—a lump-sum offer is your strongest negotiating tool. Creditors prefer immediate payment, and you can often settle the debt for a lower percentage with this approach. Use the following template as your guide. Remember to send it via certified mail with a return receipt requested to have proof of delivery.

[Your Full Name]

[Your Street Address]

[Your City, State, Zip Code]

[Your Phone Number]

[Your Email Address]

[Date]

[Creditor's Name or Collection Agency's Name]

[Creditor's Street Address]

[Creditor's City, State, Zip Code]

Re: Account Number: [Your Account Number]

To Whom It May Concern:

This letter is in regard to the outstanding balance on my account, number [Your Account Number], in the amount of $[Total Amount Owed].

Unfortunately, due to a significant change in my financial circumstances ([Briefly State Your Hardship, e.g., a recent job loss, unexpected medical expenses]), I am no longer able to make the original payments on this account. While my situation prevents me from paying the balance in full, I wish to resolve my obligation to you.

Therefore, I am writing to propose a one-time, lump-sum payment of $[Your Proposed Settlement Amount] as a settlement in full for this account. This offer represents [XX]% of the total outstanding balance. The funds for this payment are available, and I can remit them as soon as we have a signed, written agreement.

If you accept this offer, please provide a written agreement stating that this payment of $[Your Proposed Settlement Amount] will be accepted as payment in full and that the account will be considered settled. The agreement should also confirm that you will cease all collection activities and report the account to all major credit bureaus as "settled in full" or "paid as agreed."

This settlement offer is valid for a period of [e.g., 30 days] from the date of this letter. Please respond in writing to the address above.

I look forward to resolving this matter with you.

Sincerely,

[Your Signature]

[Your Printed Name]

Alternative Template: Proposing a Payment Plan

If a lump-sum payment isn't an option, proposing a structured payment plan is another viable strategy. This shows the creditor you are committed to paying off your debt over time, even with your financial hardship. This approach may result in settling for a higher overall amount than a lump-sum offer, but it can make the payments manageable.

[Your Full Name]

[Your Street Address]

[Your City, State, Zip Code]

[Your Phone Number]

[Your Email Address]

[Date]

[Creditor's Name or Collection Agency's Name]

[Creditor's Street Address]

[Creditor's City, State, Zip Code]

Re: Account Number: [Your Account Number]

To Whom It May Concern:

I am writing about my account, number [Your Account Number], which currently has an outstanding balance of $[Total Amount Owed].

My financial situation has recently changed due to [Briefly State Your Hardship, e.g., a reduction in my work hours, a family emergency]. As a result, I am unable to continue with the original payment schedule or pay the balance in full at this time. However, I am committed to fulfilling my obligation and would like to propose an alternative payment arrangement.

I would like to offer to pay a fixed amount of $[Your Proposed Monthly Payment] each month for a period of [Number of Months] months, for a total settlement of $[Total Settlement Amount]. I am prepared to make the first payment as soon as we have a formal, written agreement outlining these terms.

If you accept this payment plan, I request that you send me a written agreement confirming the terms. This agreement should state that upon completion of the payments, the account will be considered settled in full. Please also confirm that you will report the account to the credit bureaus as "paid as agreed" once the final payment is made.

Please review my proposal and respond in writing within [e.g., 30 days] to let me know if these terms are acceptable.

Thank you for your consideration. I am hopeful that we can work together to resolve this account.

Sincerely,

[Your Signature]

[Your Printed Name]

How to Send Your Letter and What to Expect Next

Writing and sending the letter is only the first step. The process that follows requires patience, persistence, and careful documentation.

Sending the Letter

Do not just drop your letter in a standard mailbox. Always send your debt negotiation letter via certified mail with a return receipt requested. This service, offered by the postal service, provides you with a mailing receipt and a record of delivery, including the recipient's signature. This documentation is your legal proof that the creditor received your offer, which is invaluable if any disputes arise later. Keep copies of the letter, the certified mail receipt, and the return receipt in a dedicated file.

Creditor Responses

After sending your letter, one of three things will likely happen:

1. Acceptance: In the best-case scenario, the creditor accepts your offer as is. They will send you the written agreement you requested. Do not send any money until you have this document in hand and have reviewed it carefully.

2. Rejection: The creditor may simply reject your offer. If this happens, don't be discouraged. You can wait a month or two and send a slightly higher offer, or you can call them to see what they might be willing to accept.

3. Counter-offer: This is the most common outcome. The creditor will respond with a counter-offer that is higher than your initial proposal but still less than the full balance. This signals that they are willing to negotiate. Now you can engage in a back-and-forth process, either by phone or in writing, until you reach a number that is acceptable to both parties.

What to Do After an Agreement is Reached

Once you and the creditor agree on a settlement amount, the most important step is to get it in writing. The written agreement should clearly state the settlement amount, the date by which it must be paid, how the account will be reported to credit bureaus, and that the payment will satisfy the debt in full. Once you have this legally-binding document, you can confidently send your payment. Be sure to pay using a traceable method, such as a cashier's check or a money order, and keep a copy for your records. Avoid giving a collection agency direct access to your bank account.

Common Mistakes to Avoid When Negotiating Debt

The debt negotiation process is filled with potential pitfalls. Avoiding these common mistakes can significantly increase your chances of a successful outcome.

- Making a Verbal Agreement: Never rely on a verbal promise from a creditor or collector. If it isn't in writing, it isn't enforceable. Always insist on a written agreement before sending any payment.

- Promising More Than You Can Afford: Be realistic about what you can pay. Defaulting on a settlement agreement can void the deal, and you may be back to owing the full original balance plus interest and fees.

- Being Dishonest About Your Hardship: While you should be concise, you must be truthful. Lying about your financial situation can undermine your credibility and cause the creditor to reject your offer.

- Ignoring Potential Tax Consequences: Remember that forgiven debt over $600 is generally considered taxable income by the IRS. Consult with a tax professional to understand how a settlement might affect your taxes.

- Giving Up Too Easily: The first offer is often just a starting point. If your initial proposal is rejected, don't be discouraged. Be prepared to negotiate and make a counter-offer if necessary. Persistence is key.

Conclusion

Taking charge of your debt through negotiation is a courageous and empowering step toward financial health. By using a structured and professional Debt Negotiation Letter Template, you can initiate a formal dialogue with your creditors and create a clear path toward a resolution. The key is to be prepared, professional, and persistent.

Remember the essential steps for success: understand your financial situation completely, choose the right template for your offer, and include all the critical elements in your letter. Always send your correspondence via certified mail to ensure a paper trail. Be prepared for a counter-offer and negotiate in good faith until you reach a realistic agreement that you can afford.

Most importantly, never send a single dollar until you have a signed, written agreement in your hands. This document is your shield and your proof of settlement. While the process requires patience, successfully negotiating your debt can lift a tremendous weight off your shoulders and set you on a firm foundation for rebuilding your financial future.

0 Response to "Debt Negotiation Letter Template"

Posting Komentar